Our FD vs Mutual Fund calculator shows, side by side, how a fixed deposit and a mutual fund could grow your money over the same period. You get a clear, number-based comparison in seconds.

Enter your amount and tenure, set the FD rate and expected fund return, and the tool reveals both outcomes — plus an optional after-tax view so the comparison is fair.

Why Compare FD and Mutual Funds?

A fixed deposit gives a guaranteed return, while a mutual fund offers higher growth potential with market risk. Choosing between them is one of the most common money decisions in India.

Seeing the two side by side helps you weigh safety against growth for your exact amount and time frame, instead of relying on rough guesses.

How to Use the FD vs Mutual Fund Calculator

- Choose a mode — monthly (SIP-style) or one-time (lump sum).

- Enter your investment amount and the number of years.

- Set the FD interest rate and your expected mutual fund return.

- Optionally turn on “Compare after tax” and pick your tax slab.

- Click Compare to see both maturity values, gains and the difference.

FD vs Mutual Fund: Key Differences

The two products differ on returns, risk, guarantee, liquidity and tax. The snapshot below sums up how they stack up.

In short, an FD trades lower returns for certainty, while a mutual fund trades certainty for higher long-term growth potential.

Advantages and Disadvantages

Fixed Deposit

- Advantages: guaranteed return, capital safety, simple to open, and insured up to ₹5 lakh per bank.

- Disadvantages: returns may barely beat inflation, interest is taxed at your slab, and early withdrawal carries a penalty.

Mutual Funds

- Advantages: higher long-term growth potential, professional management, easy SIPs, and tax-efficient equity gains.

- Disadvantages: no guarantee, values can fall, and returns depend on markets and fund selection.

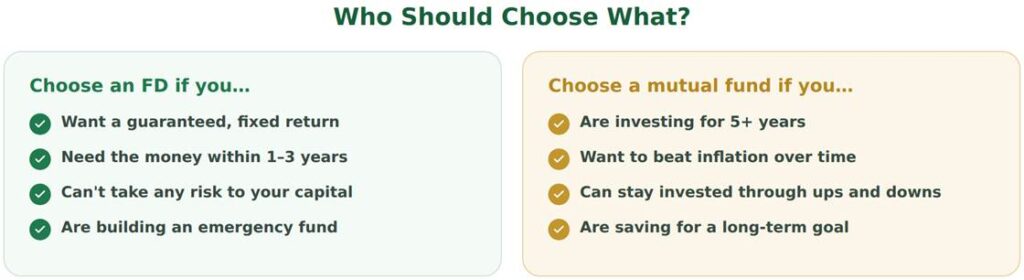

Which Is Best for Whom?

Your choice depends on how soon you need the money and how much risk you can take. Use the quick guide below.

If you lean towards safety, compare bank rates with our FD rates comparison, or build a monthly habit with our Post Office RD calculator.

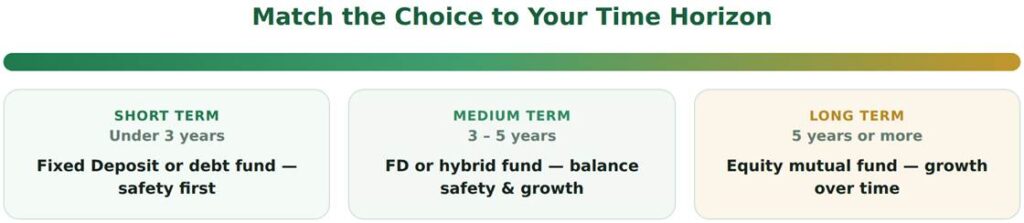

FD vs Mutual Fund by Time Period

Time horizon is the single biggest factor. Money you need soon should stay safe; money you can leave untouched can chase growth.

For under three years, an FD or debt fund is sensible. For five years or more, an equity mutual fund has more room to ride out market swings and compound.

Practical Use Cases

- Emergency fund: keep it in an FD or liquid fund for instant, safe access.

- Short goal (1–2 years): an FD protects the amount you will soon need.

- Retirement (10+ years): an equity SIP can build a larger corpus over time.

- Child’s education (8–15 years): mutual funds suit this long horizon.

- Senior citizen income: FDs, SCSS or Post Office schemes give steady, safe returns.

Taxation in the Comparison

FD interest is taxed every year at your income slab, which lowers the effective return for higher earners. Equity mutual fund gains are taxed only when you sell, at 12.5% above ₹1.25 lakh a year.

Turn on the after-tax view to see this effect. For the full rules, read our guide on tax on FD interest. You can verify mutual fund basics on the AMFI investor site.

Frequently Asked Questions (FAQs)

Is FD or mutual fund better?

It depends on your goal. An FD is better for safety and short-term needs, while a mutual fund suits long-term goals where you can accept market ups and downs for higher potential returns.

Is a mutual fund riskier than an FD?

Yes. A mutual fund is market-linked and its value can rise or fall, while an FD gives a fixed, guaranteed return with your capital protected.

Which gives higher returns, FD or mutual fund?

Historically, equity mutual funds have given higher returns than FDs over the long term, but those returns are not guaranteed. An FD gives a fixed, assured return.

How are FD and mutual fund returns taxed?

FD interest is taxed at your income slab. Equity mutual fund gains held over a year are taxed at 12.5% above ₹1.25 lakh a year.

Can I lose money in a mutual fund?

Yes, a mutual fund’s value can fall, so you can lose money, especially in the short term. An FD’s principal is safe and the return is fixed.

Should a senior citizen choose FD or mutual fund?

For safety and regular income, senior citizens usually prefer FDs, SCSS or Post Office schemes. A small mutual fund allocation can be added for long-term growth if some risk is acceptable.

Is SIP better than a recurring deposit?

For long-term goals, an equity SIP has historically outperformed an RD, but with risk. An RD gives a fixed, guaranteed maturity, which suits safety-first savers.

A fixed deposit and a mutual fund are not rivals — they solve different problems. Use this calculator to place each one where it fits your goals and time frame.