DICGC insurance covers only ₹5 lakh per bank. Learn why your ₹20 lakh FD isn’t fully protected and how to safeguard your deposits in India.

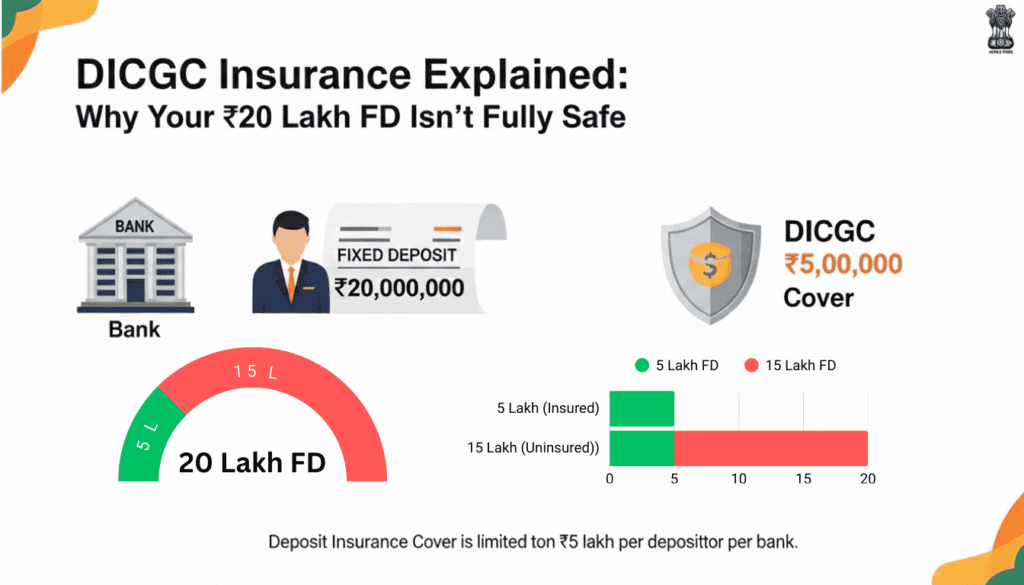

You’ve worked hard for years, saved diligently, and finally built a ₹20 lakh fixed deposit. You feel secure knowing your money is in a bank. But here’s a reality check that might shock you: if your bank fails tomorrow, you’ll only get ₹5 lakh back.

Sounds unfair? That’s exactly how thousands of PMC Bank depositors felt in 2019 when they couldn’t access their savings. The culprit? DICGC insurance limits that most people don’t understand until it’s too late.

In this guide, I’ll walk you through exactly how DICGC insurance works, why your ₹20 lakh FD isn’t as safe as you think, and most importantly—what you can do about it right now.

What is DICGC Insurance?

DICGC stands for Deposit Insurance and Credit Guarantee Corporation. It’s a wholly-owned subsidiary of the Reserve Bank of India, established in 1978 to protect depositors when banks fail.

Think of DICGC insurance as a safety net for your bank deposits. When you put money in any DICGC-insured bank in India, this insurance automatically kicks in if the bank collapses or gets merged.

The best part? You don’t pay a single rupee for this coverage. Banks pay the premium to DICGC, not you.

The ₹5 Lakh Limit: Why Your ₹20 Lakh FD is at Risk

Here’s the critical detail most people miss: DICGC insurance covers only ₹5 lakh per depositor per bank. This includes both your principal amount and the interest earned.

Let me break this down with a real example:

Example 1: Single Bank Scenario

Rajesh has the following accounts in HDFC Bank: –

- Savings Account: ₹3 lakh

- Fixed Deposit 1: ₹10 lakh –

- Fixed Deposit 2: ₹7 lakh –

If HDFC Bank fails (hypothetically), Rajesh will receive only ₹5 lakh from DICGC insurance. The remaining ₹15 lakh? It’s not covered. He might recover some amount during liquidation, but there’s no guarantee.

Example 2: Multiple Branches, Same Bank

Many people believe having FDs in different branches of the same bank provides separate coverage. This is completely wrong.

Priya has:

- FD in ICICI Andheri branch: ₹8 lakh

- FD in ICICI Mumbai Central branch: ₹6 lakh

- FD in ICICI Ghatkopar branch: ₹4 lakh

- Total in ICICI Bank: ₹18 lakh

All these deposits are aggregated. Priya’s DICGC insurance coverage? Still just ₹5 lakh across all three branches.

Real-Life Bank Failures: The PMC Bank Wake-Up Call

Let me tell you about one of India’s most devastating bank failures that proved why understanding DICGC insurance matters.

In September 2019, the RBI placed Punjab and Maharashtra Cooperative (PMC) Bank under restrictions. This was one of India’s top 10 cooperative banks with deposits worth over ₹11,000 crore.

Overnight, 9 lakh depositors couldn’t access their money. Some had their entire life savings—₹20 lakh, ₹50 lakh, even ₹1 crore—locked in this bank.

What Actually Happened to PMC Depositors?

The reality was harsh:

- Depositors with up to ₹5 lakh got their money back (eventually)

- Those with more than ₹5 lakh had to wait nearly 2.5 years (from September 2019 to March 2022) to access even their insured amount

- For amounts above ₹5 lakh, the repayment was spread over 10 years

According to official data, DICGC settled claims worth ₹3,854 crore for PMC Bank in 2022. But depositors with larger amounts are still waiting for complete recovery.

The Human Cost

Eleven people reportedly died due to the stress of not accessing their life savings. Hundreds of families faced financial devastation. Marriages were postponed. Medical treatments delayed. Retirements destroyed.

All because they didn’t understand DICGC insurance limits.

How DICGC Insurance Actually Works

Which Deposits Are Covered?

DICGC insurance covers almost all common deposit types: –

- Savings accounts

- Fixed deposits (FDs)

- Recurring deposits (RDs)

- Current accounts

- NRE, NRO, and FCNR accounts for NRIs

Which Deposits Are NOT Covered?

Here’s what DICGC doesn’t protect: –

- Deposits of central and state governments

- Interbank deposits

- Deposits of foreign governments

- Amounts due on account of deposit certificates issued by correspondents

The Principal + Interest Calculation

Many people miss this crucial point: the ₹5 lakh limit includes both principal and accrued interest.

Example: You have an FD with:

- Principal: ₹4,95,000

- Interest earned: ₹4,000

- Total: ₹4,99,000

Your entire amount is covered because it’s within ₹5 lakh.

But if you have:

- Principal: ₹5,00,000

- Interest earned: ₹72,000

- Total: ₹5,72,000

Only ₹5 lakh is insured. The ₹72,000 interest? Not covered.

The Coverage Gap: Current Data Shows the Problem

As of FY 2023-24, here are the shocking statistics from official DICGC reports:

Account Coverage:

- 98% of deposit accounts are fully covered (most people have less than ₹5 lakh)

- Only 43.1% of total deposit value is covered

- For commercial banks: 41.9% of deposits covered

- For cooperative banks: 63.3% of deposits covered

This means while most accounts are safe, more than half the actual money deposited in Indian banks isn’t fully protected.

Bank Failures Continue

According to a Ministry of Finance Parliamentary reply dated March 25, 2025:

- No commercial bank failed in the last 3 years

- 40 urban cooperative banks had their licenses cancelled in the same period

As of March 2025, 1,982 banks are insured under DICGC, including 140 commercial banks and 1,857 cooperative banks.

How to Protect Your ₹20 Lakh (Or More)

Now that you understand the risk, here’s exactly what you should do:

Strategy 1: Split Across Multiple Banks This is the most effective protection strategy.

Before (Risky): ₹20 lakh in SBI

- Protected: ₹5 lakh

- At Risk: ₹15 lakh

After (Safe): –

- ₹5 lakh in SBI

- ₹5 lakh in HDFC Bank

- ₹5 lakh in ICICI Bank

- ₹5 lakh in Axis Bank

- Protected: ₹20 lakh

- At Risk: ₹0

Each bank provides separate DICGC coverage, so your ₹20 lakh is now fully protected.

Strategy 2: Use Joint Accounts Strategically

Joint accounts get counted differently. Here’s how to maximize coverage:

In Same Bank:

- Individual account (you): ₹5 lakh covered

- Individual account (spouse): ₹5 lakh covered

- Joint account (you + spouse): ₹5 lakh covered

- Total coverage in one bank: Up to ₹15 lakh

The key is that each “capacity” gets separate coverage.

Strategy 3: Different Legal Capacities

You can increase coverage by opening accounts in different capacities:

As an individual: ₹5 lakh – As a guardian of a minor: ₹5 lakh – As a partner in a firm: ₹5 lakh – As a trustee: ₹5 lakh All in the same bank, but each capacity gets separate ₹5 lakh coverage.

Strategy 4: Monitor Interest Accruals

Remember, interest counts toward your ₹5 lakh limit. If you have a ₹4.5 lakh FD at 8% annual interest:

Year 1: Principal ₹4.5 lakh + Interest ₹36,000 = ₹4.86 lakh (Safe)

Year 2: Total becomes ₹5.23 lakh (₹23,000 not covered)

Consider withdrawing interest periodically or splitting into smaller FDs.

Is the ₹5 Lakh Limit Going to Increase?

Good news: there’s movement on this front.

In early 2025, following the New India Cooperative Bank controversy, the Centre discussed increasing DICGC insurance from ₹5 lakh to ₹8-12 lakh.

Reports suggest this change could happen by the first quarter of 2025 (though as of February 2026, it hasn’t been implemented yet).

Historical Context

The current ₹5 lakh limit was set in February 2020, increased from the earlier ₹1 lakh limit that had remained unchanged since 1993—a gap of 27 years.

Industry experts argue that ₹5 lakh is inadequate given inflation and rising income levels over the past 5 years.

The Claim Settlement Process: What to Expect

If your bank fails, here’s the timeline:

Under Current Rules (Effective September 2021)

For banks under All-Inclusive Directions (AID):

Day 1-45: Bank submits depositor list to DICGC – Day 46-90: DICGC processes and settles claims –

Total: 90 days maximum

For bank liquidation: 2 months from the date liquidator submits claim list

The Reality Check

While rules say 90 days, actual experience varies:

PMC Bank depositors waited 2.5 years for initial ₹5 lakh.

Madhavpura Mercantile Bank depositors (de-licensed in 2012) are still waiting for amounts above ₹1 lakh

The delay happens because claim settlement starts only after final resolution (merger/liquidation).

Key Questions Answered

Does DICGC cover NBFC deposits? **No.** DICGC does not cover deposits in Non-Banking Financial Companies like Bajaj Finance, Shriram Finance, or Mahindra Finance. Only RBI-regulated banks are covered.

- Are small finance banks covered?

Yes. Small finance banks like Equitas, AU, Ujjivan are DICGC-insured with the same ₹5 lakh limit.

- Do I need to file a claim?

No. The process is automatic. When a bank fails, DICGC works directly with the liquidator or successor bank. You don’t need to submit any forms.

- Can I check if my bank is DICGC-insured?

Yes. Visit the official DICGC website (www.dicgc.org.in) where they publish a regularly updated list of insured banks. As of March 2025, almost all RBI-licensed banks in India are covered.

Quick Action Checklist

Here’s what you should do today:

✓ Calculate Total: Add up all your deposits in each bank (including interest).

✓ Identify Risk: Find banks where you have more than ₹5 lakh total.

✓ Split Immediately: If you have ₹20 lakh in one bank, split it across 4 different banks.

✓ Review Annually: Interest accruals can push you over ₹5 lakh—check every year.

✓ Verify Coverage: Check if your bank is on the DICGC insured list.

✓ Avoid NBFCs: For large amounts, stick to DICGC-insured banks, not NBFCs.

✓ Document Everything: Keep all FD receipts, account statements, and nomination details updated.

Common Mistakes to Avoid

Mistake 1: “Different branches = Different coverage” Wrong. All branches of the same bank are clubbed together.

Mistake 2: “My bank is too big to fail.” PMC was a top 10 cooperative bank. Yes Bank, a listed commercial bank, faced a crisis in 2020. Size doesn’t guarantee safety.

Mistake 3: “DICGC covers everything” No. Only ₹5 lakh per depositor per bank, including interest.

Mistake 4: “I’ll get my money immediately” Even insured amounts can take months or years. PMC depositors waited 2.5 years.

Mistake 5: “Higher interest rates are always better” Higher rates often come from riskier banks. Balance return with safety.

Comparison: India vs Other Countries

| Country | Deposit Insurance Limit | Coverage (USD Equivalent) |

| India (DICGC) | ₹5 lakh | ~$6,000 |

| USA (FDIC) | $250,000 | ~$250,000 |

| UK (FSCS) | £85,000 | ~$105,000 |

| Singapore (SDIC) | SGD 100,000 | ~$75,000 |

| Australia | AUD 250,000 | ~$165,000 |

India’s coverage is significantly lower than developed economies, even accounting for cost of living differences.

Final Thoughts: Your Money, Your Responsibility

DICGC insurance is a crucial safety net, but it’s not a complete solution. The ₹5 lakh limit hasn’t kept pace with inflation or rising incomes.

If you have ₹20 lakh, ₹50 lakh, or more in fixed deposits, spreading it across multiple banks isn’t just smart—it’s essential. Don’t wait for a PMC Bank-like crisis to hit your bank before taking action.

Your hard-earned money deserves better protection. Take 30 minutes today to review your deposits and make the necessary splits. Your future self will thank you.

Frequently Asked Questions

1. What happens if I have ₹10 lakh in one bank?

If the bank fails, DICGC will cover only ₹5 lakh. The remaining ₹5 lakh depends on the bank’s liquidation proceeds, which can take years and might result in partial or zero recovery.

2. Is DICGC insurance automatic or do I need to apply?

It’s completely automatic. You don’t need to apply, pay premiums, or file claims. Banks pay DICGC premiums, and if a bank fails, DICGC settles claims through the liquidator or successor bank.

3. Can I have multiple ₹5 lakh FDs in different banks for full protection?

Yes! This is the recommended strategy. Each bank provides separate DICGC coverage. If you have ₹20 lakh, split it into four ₹5 lakh FDs across four different banks for complete protection.

4. Does DICGC cover corporate FDs from companies like Bajaj Finance?

No. DICGC only covers deposits in RBI-regulated banks. Corporate FDs, NBFC deposits, mutual funds, and bonds are not covered under DICGC insurance.

5. How long does it take to get my insured amount if a bank fails?

Officially, DICGC must settle claims within 90 days for banks under RBI directions, and 2 months for liquidated banks. However, in reality, it can take 6 months to 2-3 years depending on the resolution process.

6. Will the DICGC limit increase from ₹5 lakh soon?

There are discussions to increase it to ₹8-12 lakh as of early 2025, but no official implementation yet. The last increase from ₹1 lakh to ₹5 lakh happened in February 2020 after 27 years. Don’t wait for an increase—protect your deposits now.