The FD Dilemma Most Indians Face

You’ve worked hard, saved some money, and now you want to put it somewhere safe — somewhere it quietly grows without keeping you up at night. You’ve heard people talk about fixed deposits. But then comes the question that trips up almost every first-time investor: Should I go with a bank FD or a post office FD?

It’s a fair question, and honestly, the answer isn’t the same for everyone. When comparing bank FD vs post office FD, both options offer guaranteed returns and capital protection — but they differ in ways that can actually matter to your financial goals.

In this guide, we’ll break down everything — the bank FD vs post office FD interest rate, safety levels, tax treatment, and who should pick what — all using live 2026 data.

Let’s get into it.

What Is a Post Office FD (Time Deposit)?

The post office FD scheme is officially called the National Savings Time Deposit Account, run by India Post under the Ministry of Finance. It’s one of India’s oldest small savings instruments — trusted by millions of households across the country.

Here’s the basic idea: you deposit a lump sum at your nearest post office (or online via India Post’s portal), lock it in for a set period, and earn a fixed rate of interest. Simple, safe, and government-backed.

Key features of post office FD in 2026:

- Minimum deposit: ₹1,000 (in multiples of ₹100)

- Post office FD maximum limit: No upper cap — you can deposit as much as you want

- Tenure options: 1, 2, 3, and 5 years only

- Interest compounded quarterly, paid annually

- 5-year FD qualifies for tax deduction under Section 80C

- No TDS deducted at source (but you must declare interest in your ITR)

- Available at 1.6 lakh+ post offices across India

What Is a Bank FD?

A bank fixed deposit works similarly — you deposit money for a fixed period and earn guaranteed returns. But unlike post offices, banks are regulated by the Reserve Bank of India (RBI) and offer much more flexibility in tenure and access.

Key features of a bank FD:

- Tenures ranging from 7 days to 10 years

- Higher flexibility in choosing tenure

- Online opening and management (net banking, mobile apps)

- TDS deducted if annual interest exceeds ₹40,000 (₹50,000 for senior citizens)

- Senior citizens get an additional 0.50% interest benefit at most banks

- Deposits insured up to ₹5 lakh under DICGC (Deposit Insurance and Credit Guarantee Corporation)

Bank FD vs Post Office FD Interest Rate: 2026 Comparison

This is where the rubber meets the road. Let’s look at the live rates for Q1 2026.

Post Office FD Interest Rates (Jan–Mar 2026)

Post Office FD interest rates range from 6.90% to 7.50% p.a. effective from January 1, 2026, to March 31, 2026, depending on the tenure. The government reviews these quarterly.

| Tenure | Post Office FD Rate (General & Senior Citizens) |

|---|---|

| 1 Year | 6.90% p.a. |

| 2 Years | 7.00% p.a. |

| 3 Years | 7.10% p.a. |

| 5 Years | 7.50% p.a. |

Note: Unlike banks, India Post does not offer preferential rates for senior citizen depositors.

SBI Bank FD Interest Rates (2026)

The current SBI FD rates for regular citizens range from 3.05% to 6.45%, and for senior citizens, they range from 3.55% to 6.95%.

| Tenure | SBI Rate (General) | SBI Rate (Senior Citizens) |

|---|---|---|

| 1 Year | ~5.90% p.a. | ~6.40% p.a. |

| 2–3 Years | ~6.30–6.40% p.a. | ~6.80–6.90% p.a. |

| 5 Years | ~6.05% p.a. | ~7.05% p.a. |

| 444 Days (Amrit Vrishti) | 6.45% p.a. | 6.95% p.a. |

Quick takeaway: For long-term deposits, the post office FD vs bank FD interest rate comparison clearly shows the post office wins — offering 7.50% vs SBI’s 6.05% for a 5-year tenure for general investors.

Full Comparison Table: Bank FD vs Post Office FD (2026)

| Parameter | Post Office FD | Bank FD (e.g., SBI) |

|---|---|---|

| Interest Rate (5 Yr) | 7.50% p.a. | 6.05–6.40% p.a. |

| Safety | Sovereign Government Guarantee | DICGC Insurance (up to ₹5 lakh) |

| Senior Citizen Benefit | None | +0.50% extra |

| Minimum Deposit | ₹1,000 | ₹1,000 |

| Maximum Limit | No limit | No limit |

| Tenure Flexibility | 1, 2, 3, 5 years only | 7 days to 10 years |

| TDS | Not deducted | Deducted above ₹40,000 |

| Tax Benefit (80C) | Yes (5-year FD) | Yes (5-year Tax Saver FD) |

| Online Opening | Yes (India Post portal) | Yes (net banking/app) |

| Premature Withdrawal | Allowed after 6 months (penalty applies) | Allowed (0.5%–1% penalty) |

| Compounding | Quarterly | Quarterly |

| Loan Against FD | Yes | Yes (up to 90% of deposit) |

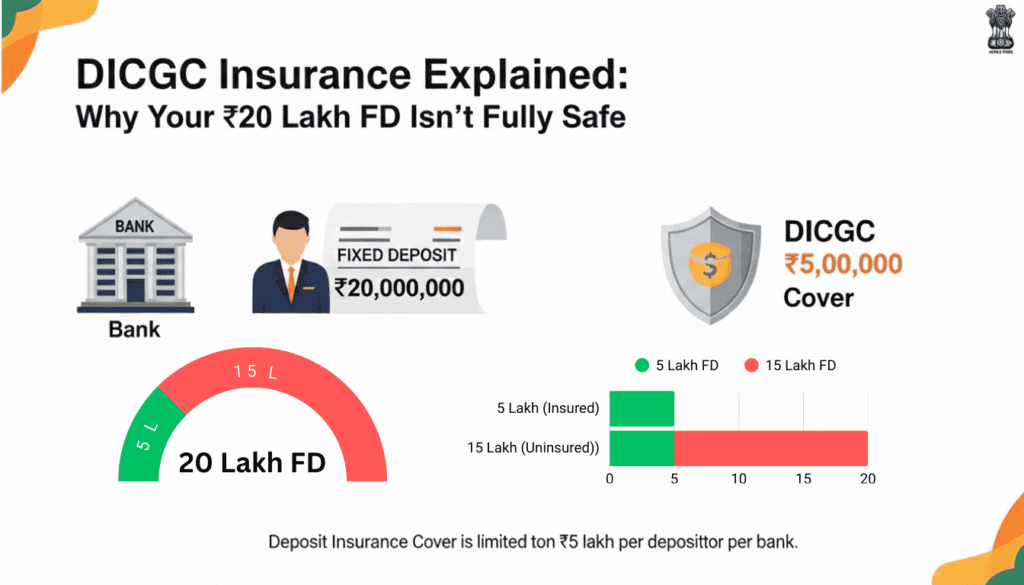

Which Is Safer: Post Office FD or Bank FD?

This is the question retirees and risk-averse investors ask the most — and it’s a very valid one.

Post Office FD safety: Post Office FDs offer a sovereign guarantee — meaning the full deposit is backed by the Government of India. There’s no cap on the guaranteed amount. Whether you deposit ₹1 lakh or ₹50 lakh, every rupee is protected.

Bank FD safety: The Deposit Insurance Scheme of the RBI covers all bank deposits up to ₹5,00,000. This means if a bank fails, you’re protected only up to ₹5 lakh — anything above that is at risk, at least in theory.

Verdict: For deposits above ₹5 lakh, post office FDs are technically safer. For amounts below ₹5 lakh, both are effectively safe for most practical purposes.

Practical Example: ₹1 Lakh and ₹3 Lakh FD in Post Office vs Bank

Let’s calculate so you can see the difference in real money.

1 Lakh FD Interest in Post Office (5 Years at 7.50%)

Using quarterly compounding:

- Principal: ₹1,00,000

- Rate: 7.50% p.a.

- Tenure: 5 years

- Estimated Maturity Amount: ~₹1,43,000

- Total Interest Earned: ~₹43,000

3 Lakh FD Interest in Post Office (5 Years at 7.50%)

- Principal: ₹3,00,000

- Rate: 7.50% p.a.

- Tenure: 5 years

- Estimated Maturity Amount: ~₹4,29,000

- Total Interest Earned: ~₹1,29,000

SBI Bank FD — 1 Lakh (5 Years at 6.05%)

- Principal: ₹1,00,000

- Rate: 6.05% p.a.

- Tenure: 5 years

- Estimated Maturity Amount: ~₹1,34,600

- Total Interest Earned: ~₹34,600

The difference? Over 5 years, you earn roughly ₹8,400 more on ₹1 lakh with the post office than with SBI. Scale that up to ₹3 lakh, and you’re looking at a gap of ~₹25,000+ — not something to ignore.

💡 Pro Tip: Use a bank FD vs post office FD calculator online to compute your exact maturity value based on your deposit amount and chosen tenure.

Post Office FD vs Bank FD: Who Should Choose What?

Choose Post Office FD If You:

- Are a retiree or conservative investor who wants the absolute safest option

- Are depositing more than ₹5 lakh and don’t want to worry about DICGC limits

- Want higher guaranteed returns without market risk

- Are looking for a 5-year tax-saving FD with the highest possible rate

- Are a salaried professional in a lower tax bracket looking for long-term savings

Choose Bank FD If You:

- Are a senior citizen (banks give 0.50% extra — post offices don’t)

- Need shorter tenures like 7 days, 3 months, or 6 months

- Prefer 100% online management through mobile banking

- Want to start an SBI bank FD vs post office FD comparison for your specific bank’s special schemes

- Need a loan against FD quickly and easily

Bank FD vs Post Office RD, MIS, and Time Deposit: Quick Overview

Many investors confuse these related instruments. Here’s a quick snapshot:

- Bank FD vs Post Office Time Deposit (TD): Post Office TD is the same as Post Office FD — these terms are used interchangeably. The TD offers 6.90%–7.50%.

- Bank FD vs Post Office RD (Recurring Deposit): Post Office RD lets you invest a small amount monthly, currently at 6.70% p.a. Bank RDs are more flexible but often offer lower rates.

- Bank FD vs Post Office MIS (Monthly Income Scheme): If you want monthly payouts from your lump sum, the Post Office MIS (National Savings Monthly Income Account) offers fixed monthly income and is ideal for investors seeking regular income from a lump-sum investment. The MIS maximum limit is ₹9 lakh for a single account and ₹15 lakh for a joint account.

Tax Treatment: A Factor You Can’t Ignore

Both bank and post office FDs are taxable, but there’s one key operational difference:

- Bank FD: TDS is automatically deducted if interest exceeds ₹40,000 per year (₹50,000 for senior citizens). You can submit Form 15G/15H to avoid TDS if your total income is below the taxable limit.

- Post Office FD: The Post Office does not deduct TDS — but you must account for interest income in your tax returns. This means better cash flow throughout the year, but you need to be disciplined about self-reporting.

For the 5-year FD, both bank and post office deposits qualify for deduction up to ₹1.5 lakh under Section 80C.

Benefits Summary: Post Office FD

- ✅ Backed by the Government of India — zero default risk

- ✅ Highest interest rate among safe fixed-income products (up to 7.50%)

- ✅ No TDS deduction — better liquidity management

- ✅ No maximum deposit limit

- ✅ Tax benefit on 5-year FD under Section 80C

- ✅ Available at 1.6 lakh+ post offices across India — even in rural areas

Benefits Summary: Bank FD

- ✅ Extra 0.50% for senior citizens

- ✅ More tenure flexibility (7 days to 10 years)

- ✅ Fully digital — open, manage, and close online

- ✅ Special schemes (SBI Amrit Vrishti — 6.45% for 444 days)

- ✅ Loan up to 90% of FD value available

- ✅ Trusted and convenient for urban investors

FAQs: Bank FD vs Post Office FD

1. Which is better — post office FD or bank FD?

It depends on your goal. If you want higher returns and maximum safety, post office FD at 7.50% (5 years) is better. If you’re a senior citizen or need more flexibility in tenure, a bank FD may suit you better due to the 0.50% extra rate and digital convenience.

2. What is the post office FD interest rate in 2026?

Post office FD interest rates in 2026 range from 6.90% to 7.50% p.a., effective January 1 to March 31, 2026. The 5-year post office FD offers the highest rate at 7.50%.

3. Is post office FD safer than bank FD?

Yes, technically. Post office FDs carry a full sovereign government guarantee with no upper limit. Bank FDs are insured only up to ₹5 lakh under DICGC. For large deposits, post office FDs are safer.

4. What is the maximum limit for post office FD?

There is no maximum deposit limit for post office FD. You can invest any amount above ₹1,000, in multiples of ₹100.

5. How much interest will I get on ₹1 lakh FD in a post office?

At 7.50% for 5 years with quarterly compounding, a ₹1 lakh post office FD will grow to approximately ₹1,43,000 at maturity — earning around ₹43,000 in interest.

6. Does post office FD offer senior citizen benefits?

No. Unlike banks, India Post does not offer any additional interest rate for senior citizens. All depositors get the same rate regardless of age.

7. Is TDS deducted on post office FD?

No, TDS is not deducted on post office FDs. However, the interest earned is taxable and must be declared in your Income Tax Return (ITR) as per your applicable slab.

8. Can I open a post office FD online?

Yes. You can open a Post Office FD online if you have a linked India Post Savings Account. However, first-time investors may need to visit a branch for KYC and account activation.

Conclusion: Which FD Should You Pick in 2026?

Let’s sum it up simply.

If you’re someone who values safety above everything, is investing for the long term (5 years), and doesn’t need the money in between — the post office FD is hands down the better choice in 2026. With 7.50% vs SBI’s 6.05%, the difference in returns is real and meaningful.

If you’re a senior citizen, need short-term investment options, or love the convenience of managing everything digitally — a bank FD from a trusted public sector bank is perfectly fine.

The good news? You don’t always have to choose just one. Many smart investors split their corpus — parking a portion in post office FDs for safety and higher returns, and keeping some in bank FDs for flexibility and easy access.

Before you invest, always:

- Use a bank FD vs post office FD calculator to estimate your actual maturity amount

- Check the latest quarterly rates — post office rates are reviewed every 3 months

- Consider your tax bracket, because post-tax returns matter more than headline rates

Whatever you choose — invest with purpose, stay informed, and let your money do the hard work for you.

Disclaimer: Interest rates mentioned are as per publicly available data for Q1 2026 (January–March 2026). Rates are subject to revision. Please verify the latest rates at your bank or the official India Post website before investing. This article is for informational purposes only and does not constitute financial advice.