Introduction: Which Fixed-Income Option Actually Works for You?

If you’ve ever sat with a cup of chai wondering where to park your hard-earned savings — you’re not alone. Most Indians default to a bank FD without even considering other options. But here’s the thing: when you compare Bank FD vs Corporate FD vs Bonds, the differences in returns, safety, and flexibility can genuinely change your financial future.

This guide is your one-stop reference — a clear, jargon-free breakdown of all three options, including a full comparison table, real examples, and answers to the questions most investors are too nervous to ask.

What Exactly Are These Three Instruments?

Bank Fixed Deposit (FD)

A Bank FD is the most familiar savings tool in India. You deposit a lump sum with a bank for a fixed tenure, and you earn guaranteed interest. Banks like Axis Bank, SBI, HDFC, and ICICI offer FD rates typically ranging from 6.5% to 7.5% per annum as of 2024–25.

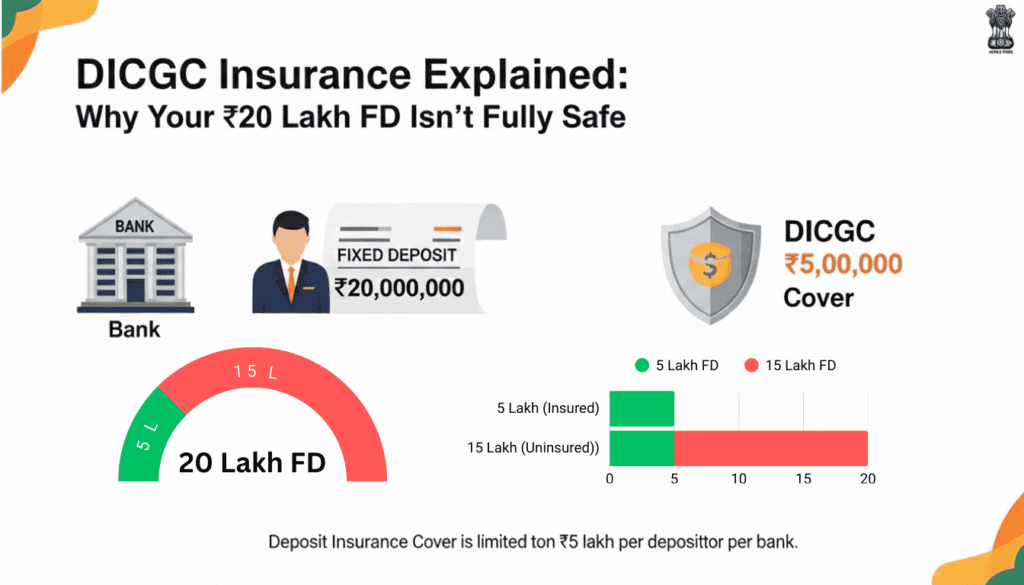

What makes bank FDs special is the safety net: deposits up to ₹5 lakh are insured by DICGC (Deposit Insurance and Credit Guarantee Corporation). So even if the bank fails (which is rare), your money up to that limit is protected.

Corporate Fixed Deposit (FD)

Corporate FDs work similarly to bank FDs — you deposit money with a company (like Bajaj Finance, Mahindra Finance, or Shriram Finance) for a fixed period and earn interest. The catch? Returns are higher — often 7.5% to 9% per annum — but there’s no DICGC insurance.

The safety depends entirely on the company’s credit rating. Always look for AAA-rated corporate FDs to minimize risk.

Bonds

Bonds are debt instruments where you lend money to a government or corporation in exchange for periodic interest payments (called coupon payments) and the return of principal at maturity. In India, you can invest in:

- Government Bonds – Issued by the RBI or state governments. Virtually risk-free.

- RBI Floating Rate Savings Bonds – Interest rate linked to NSC rates, currently around 8.05%, revised every 6 months.

- Corporate Bonds – Issued by companies; higher yield but higher risk.

Bank FD vs Corporate FD vs Bonds: The Complete Safety & Returns Matrix

Here’s the comparison table you’ve been waiting for:

| Feature | Bank FD | Corporate FD | Government Bond | Corporate Bond |

| Returns (approx.) | 6.5%–7.5% | 7.5%–9% | 7%–8.05% | 7%–11% |

| Safety | High (DICGC up to ₹5L) | Moderate (rating-dependent) | Very High | Moderate to Low |

| Liquidity | Medium (premature penalty) | Low (lock-in) | High (tradeable) | Medium |

| Taxation | Interest fully taxable | Interest fully taxable | Interest fully taxable | Interest fully taxable |

| Minimum Investment | ₹1,000 | ₹5,000–₹10,000 | ₹1,000 | ₹1,000–₹10,000 |

| DICGC Insurance | Yes | No | No (sovereign guarantee) | No |

| Ideal For | All investors | Moderate risk-takers | Retirees, conservative | Aggressive investors |

Corporate Bond Fund vs FD: What’s the Difference?

A lot of investors mix up corporate bond fund vs FD. Let’s clear this up simply.

A Corporate Bond Fund is a mutual fund that pools money and invests in multiple corporate bonds. Unlike a Corporate FD where you lock in at one rate, a bond fund’s NAV fluctuates daily based on market conditions.

- Corporate FD: Fixed, guaranteed return. Suitable if you want certainty.

- Corporate Bond Fund: Market-linked returns. Can give 8%–10% CAGR over 3+ years, but returns aren’t guaranteed.

If you’re okay with some NAV movement and want tax efficiency through indexation (for older investments), bond funds can be smarter for 3-year+ horizons. For short-term or capital preservation, stick to a Corporate FD with an AAA rating.

RBI Floating Rate Savings Bonds vs Fixed Deposit

This is one of the most searched questions — RBI Floating Rate Savings Bonds vs Fixed Deposit — and for good reason.

Here’s a quick head-to-head:

- RBI Floating Rate Bonds currently offer 8.05% p.a., paid semi-annually, with a 7-year lock-in period. The rate resets every 6 months based on NSC rates.

- Bank FDs offer 6.5%–7.5%, with flexible tenures from 7 days to 10 years.

Who should choose RBI Bonds? Retirees or conservative investors who want a higher, government-backed return and don’t need liquidity for 7 years.

Who should stick to FD? Salaried professionals or anyone needing flexible access to their funds.

Fixed Deposit vs Bonds India: Which is Better?

The honest answer: it depends on your goal.

Choose Fixed Deposits if:

- You need capital safety above everything.

- Your investment horizon is short (1–3 years).

- You’re a first-time investor or senior citizen (many banks offer extra 0.25%–0.5% for senior citizens).

- You want simplicity with no market risk.

Choose Bonds if:

- You want higher returns and can tolerate minor market risk.

- Your investment horizon is 5–10 years.

- You want to diversify beyond bank instruments.

- You’re comfortable with government or high-rated corporate issuers.

A Practical Example: ₹5 Lakh Investment Over 5 Years

Let’s say Priya, a 35-year-old salaried professional from Pune, invests ₹5 lakh for 5 years.

| Option | Rate | Approx. Returns (5 Years) | Maturity Amount |

| Bank FD (SBI) | 7% | ₹2,01,359 | ₹7,01,359 |

| Corporate FD (Bajaj) | 8.35% | ₹2,47,500 | ₹7,47,500 |

| RBI Floating Rate Bond | 8.05% | ₹2,36,000 | ₹7,36,000 |

| Corporate Bond Fund | ~9% (est.) | ₹2,69,000 | ₹7,69,000 |

Returns are approximate and for illustration only. Actual returns may vary.

Priya notices that while the Bank FD is the safest, she’s leaving almost ₹68,000 on the table over 5 years compared to a Corporate Bond Fund. The question is: is that safety worth ₹68,000 to her?

Key Benefits at a Glance

Bank FD Benefits:

- DICGC insurance up to ₹5 lakh

- Easy to open (even online)

- Senior citizen benefits available

- No market risk

Corporate FD Benefits:

- Higher interest rates than bank FDs

- Fixed returns, no NAV volatility

- Accessible from NBFCs with strong ratings

Bond Benefits:

- Can be traded on the secondary market

- Government bonds are sovereign-guaranteed

- RBI bonds offer better returns than most bank FDs

- Bond funds offer indexation benefit (for older investments)

Fixed Deposit Plus Axis Bank: A Quick Note

If you’re banking with Axis Bank, their Fixed Deposit Plus offering is worth knowing. It combines a regular FD with an overdraft facility, meaning your money earns FD interest while also being available as a credit line in emergencies. This is particularly useful for salaried individuals who want both safety and liquidity.

Axis Bank’s FD rates currently range from 3% to 7.2% depending on tenure.

Documents Required for FD

Opening an FD is simple. Here’s what you’ll typically need:

- PAN Card

- Aadhaar Card (for KYC)

- Passport-size photograph

- Existing savings account with Axis Bank (for seamless transfer)

- Form 15G/15H (if you want to avoid TDS — for individuals with income below taxable threshold)

Most of this can be done online via the Axis Bank mobile app or net banking in under 10 minutes.

Tips Before You Invest

- Never put more than ₹5 lakh in a single bank FD if safety is your priority — that’s the insurance limit.

- Always check credit ratings before investing in Corporate FDs or Bonds. Stick to AAA or AA+ ratings.

- Ladder your FDs — split your corpus into multiple FDs with different maturities so you always have liquidity.

- Factor in taxes — interest from FDs and bonds is added to your income and taxed at your slab rate. For bond funds held 3+ years, older tax rules offered indexation; check current tax rules before investing.

- Compare real returns — if inflation is 5% and your FD gives 7%, your real return is only 2%.

FAQs: Bank FD vs Corporate FD vs Bonds

Q1. Which is safer — Bank FD or Corporate FD? Bank FD is safer because it comes with DICGC insurance up to ₹5 lakh. Corporate FDs are not insured, so if the company defaults, your money is at risk. Always choose Corporate FDs from AAA-rated companies only.

Q2. Are RBI Floating Rate Savings Bonds better than Fixed Deposits? For long-term investors (7-year horizon) who want safety and higher returns, RBI Bonds at 8.05% are better than most bank FDs. However, they lack liquidity due to the 7-year lock-in, which makes them unsuitable for short-term goals.

Q3. What is a fixed deposit bond? A “fixed deposit bond” is not a standardized term in India. It loosely refers to either a Corporate FD or a government savings bond — both offer fixed returns over a defined period. Context matters, so always check the issuer before investing.

Q4. Is corporate bond fund better than FD for tax purposes? For investments held over 3 years (under older rules), corporate bond funds offered indexation benefits that reduced tax. However, as per recent changes in India’s tax rules, debt mutual fund gains are now taxed at your income slab rate regardless of holding period. Consult a financial advisor for current tax treatment.

Q5. Which is better than fixed deposit for higher returns? Corporate FDs, RBI Floating Rate Bonds, and Corporate Bond Funds all potentially offer higher returns than a regular bank FD. The trade-off is reduced safety or liquidity. For a balanced approach, consider splitting your corpus across a Bank FD and an RBI Bond.

Q6. What documents are required for FD in Axis Bank? You need a PAN Card, Aadhaar Card, a photograph, and an existing Axis Bank account. Form 15G/15H can be submitted to avoid TDS if your income is below the taxable limit.

Conclusion: Make the Right Choice for Your Financial Goals

The debate around Bank FD vs Corporate FD vs Bonds doesn’t have a single winner — it depends entirely on your risk appetite, investment horizon, and financial goals.

If safety is non-negotiable, stick to Bank FDs or RBI Savings Bonds. If you want better returns and can handle moderate risk, Corporate FDs (from top-rated NBFCs) and bond funds are worth exploring. And if you’re building a long-term retirement corpus, a mix of all three — laddered strategically — often delivers the best result.

The smartest investors don’t put all their eggs in one basket. They compare, diversify, and review regularly.