Sakthi Finance Fd interest Rates 2026- Earn upto 11.21%

(1)")

Let’s be honest — parking your savings in a regular bank FD that gives you 6–7% is starting to feel like leaving money on the table.

If you’ve been searching for better fixed deposit options with a trusted NBFC, you’ve probably come across Sakthi Finance FD interest rates in your research. And there’s a good reason for that — this South India-based NBFC has been around since 1955 and still offers some genuinely competitive rates.

In this guide, we’re going to break everything down for you — the exact interest rates, how their deposit schemes work, who can invest, what makes them different from bank FDs, and whether it makes sense for your specific financial situation.

Whether you’re a salaried professional looking to diversify, a retiree wanting a dependable monthly income, or simply someone who wants their savings to do more — this article is for you.

Let’s get into it.

Who Is Sakthi Finance? A Quick Background

Before you put your money anywhere, you want to know who you’re trusting it with. Fair enough.

Sakthi Finance Limited has been operating since 1955, starting out as the Pollachi Credit Society Private Limited, headquartered in Pollachi, Tamil Nadu. Over seven decades, it evolved into one of the leading NBFCs (Non-Banking Financial Companies) in South India.

Today, Sakthi Finance primarily specialises in financing used commercial vehicles and construction equipment, and has a network of more than 50 branches spread across Andhra Pradesh, Karnataka, Kerala, Tamil Nadu, and Telangana.

For investors, Sakthi Finance offers Fixed Deposit schemes through its authorised distributor, Sakthi Financial Services.

The company is part of the larger Sakthi Group — a well-established conglomerate in South India — which adds a layer of credibility and institutional backing that many smaller NBFCs simply can’t offer.

In short: this isn’t a fly-by-night company. It has decades of history, a regulated structure, and a real track record.

Understanding Sakthi Finance FD Interest Rates 2026

Now let’s talk numbers — because that’s probably why you’re here.

Sakthi Finance offers two deposit schemes: Fixed Income (Scheme I) and Cumulative Income (Scheme II), with deposit terms ranging from 15 months to 60 months.

Sakthi Finance FD Rates — Regular Investors (Effective from 07.08.2023)

")

Here’s the complete interest rate table for regular (non-senior citizen) investors:

| Term (Months) | Interest Rate p.a. (%) | Monthly Payout (%) | Quarterly Payout (%) | Annual Yield (%) | Maturity Amount (per ₹10,000) |

| 15 Months | 8.25% | 8.25% | 8.25% | 8.60% | ₹11,075 |

| 24 Months | 8.50% | 8.50% | 8.50% | 9.16% | ₹11,832 |

| 36 Months | 8.75% | 8.75% | 8.75% | 9.88% | ₹12,965 |

| 48 Months | 9.00% | 9.00% | 9.00% | 10.69% | ₹14,276 |

| 60 Months | 9.00% | 9.00% | 9.00% | 11.21% | ₹15,605 |

Minimum deposit for monthly payouts: ₹25,000 | For quarterly & cumulative: ₹10,000

Sakthi Finance FD Rates — Senior Citizens (Effective from 07.08.2023)

Senior citizens get an extra 0.25% on every tenure. Here’s their rate card:

| Term (Months) | Interest Rate p.a. (%) | Monthly Payout (%) | Quarterly Payout (%) | Annual Yield (%) | Maturity Amount (per ₹10,000) |

| 15 Months | 8.50% | 8.50% | 8.50% | 8.87% | ₹11,109 |

| 24 Months | 8.75% | 8.75% | 8.75% | 9.45% | ₹11,890 |

| 36 Months | 9.00% | 9.00% | 9.00% | 10.20% | ₹13,061 |

| 48 Months | 9.25% | 9.25% | 9.25% | 11.04% | ₹14,416 |

| 60 Months | 9.25% | 9.25% | 9.25% | 11.59% | ₹15,797 |

Minimum deposit: ₹10,000 (quarterly/cumulative) | ₹25,000 (monthly)

These Sakthi Finance FD rates are noticeably higher than what most nationalised banks currently offer — and that’s the key appeal for savvy investors.

Sakthi Finance FD vs Bank FD: A Real Comparison

Let’s put things side by side so you can see the difference clearly.

| Feature | Sakthi Finance FD | Typical Bank FD (SBI/PNB) |

| Interest Rate (3 years) | 8.75% | ~6.50–7.00% |

| Senior Citizen Benefit | +0.25% | +0.25–0.50% |

| Minimum Deposit | ₹10,000 | ₹1,000 |

| Tenure Options | 15, 24, 36, 48, 60 months | Flexible (7 days to 10 years) |

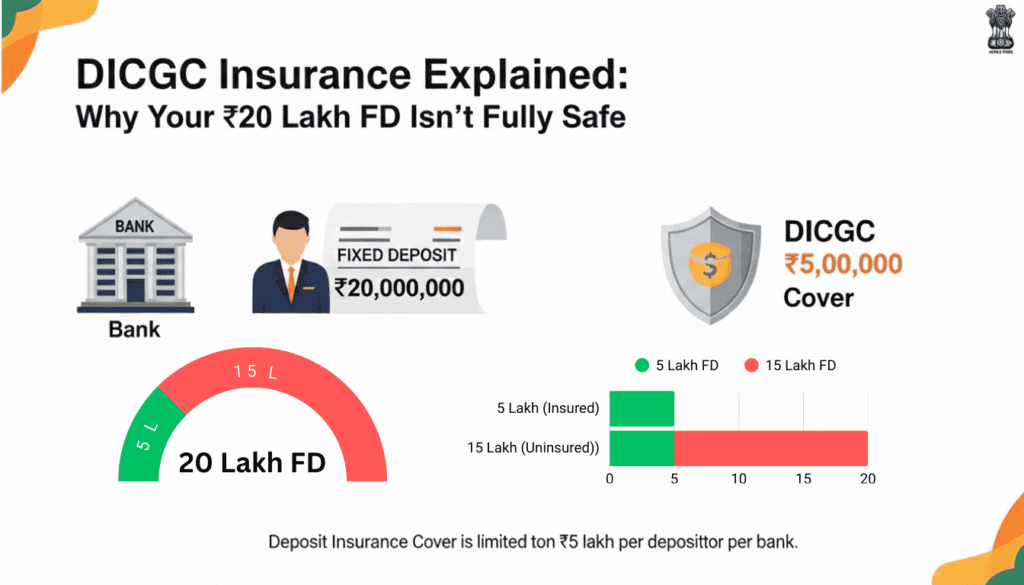

| Deposit Insurance (DICGC) | Not covered (NBFC) | Covered up to ₹5 lakhs |

| Regulated By | RBI (as NBFC) | RBI (as Bank) |

| Premature Withdrawal | Allowed (with conditions) | Allowed (with penalty) |

| Interest Payout Options | Monthly / Quarterly / Cumulative | Monthly / Quarterly / Cumulative |

Key Takeaway: You earn meaningfully more with Sakthi Finance, but unlike bank FDs, the deposits are not covered under DICGC insurance. That’s the trade-off — higher return, slightly higher risk profile. This is true of all NBFC FDs in India.

How the Two FD Schemes Work — Scheme I & Scheme II

Sakthi Finance keeps things simple with two primary options:

Scheme I: Fixed Income (Interest Payout)

This is ideal if you want regular cash flow — like a monthly or quarterly income supplement.

You deposit a lump sum, and Sakthi Finance pays you interest at regular intervals — either monthly or quarterly — directly into your bank account.

Best for: Retirees, homemakers, anyone who wants a secondary income stream without touching the principal.

Example: If you invest ₹5,00,000 in the 60-month scheme at 9.00% per annum, you receive approximately ₹3,750 every month for 5 years. At maturity, your ₹5 lakhs comes back to you.

Scheme II: Cumulative Income

Here, interest gets compounded and paid out at maturity. You don’t receive any payouts during the tenure — instead, the interest rolls over and grows.

Best for: Salaried professionals, younger investors, people building a corpus for a goal (child’s education, house down payment, retirement).

Example: ₹10,000 invested for 60 months at 9.00% p.a. grows to ₹15,605 at maturity. That’s 56% growth on your investment.

Sakthi Finance NCD: Another Way to Invest

Apart from fixed deposits, Sakthi Finance also offers Non-Convertible Debentures (NCDs) — which is another investment instrument worth knowing about.

Non-Convertible Debentures are secured financial instruments that cannot be converted into equity or preference shares, and carry a fixed tenure and rate of interest.

Sakthi Finance NCD issues have been done regularly — in 2019, 2020, 2021, 2022, 2023, 2024 (twice), 2025, and even a July 2025 issue is available. These are listed on stock exchanges, making them relatively liquid compared to FDs.

Sakthi Finance Subordinated Bond

In addition to NCDs, they also offer a Subordinated Bond — a more specialized fixed-income instrument.

The Subordinated Bond from Sakthi Finance comes with a minimum investment of ₹50,000, a tenure of 61 months, a fixed interest rate of 10%, and a cumulative yield of 12.83%.

This is a private placement product — meaning it’s available to specific, qualified investors and not the general public.

FD vs NCD vs Subordinated Bond: Which One Is Right for You?

| Product | Min. Investment | Tenure | Rate | Who It’s For |

| Fixed Deposit | ₹10,000 | 15–60 months | 8.25–9.00% | General public |

| NCD | Varies by issue | Fixed per issue | Market-linked | Investors comfortable with exchange-listed instruments |

| Subordinated Bond | ₹50,000 | 61 months | 10% fixed | HNIs / specific investors |

Who Can Invest in Sakthi Finance FD?

The categories of investors permitted to invest in Sakthi Finance FDs include Individuals, Partnership Firms, Companies, Trusts, Associations, and HUFs (Hindu Undivided Families).

The deposit application also allows up to 3 joint applicants — so a couple or family members can jointly hold a deposit, which is a useful feature for estate planning.

How to Open a Sakthi Finance Fixed Deposit: Step-by-Step

The process is straightforward. Here’s how it works:

Step 1: Get the Application Form Download or collect the deposit application form from Sakthi Finance’s authorised distributor — Sakthi Financial Services — or visit a branch near you.

Step 2: Fill in the Form Complete the application form with your personal details, nominee information, joint applicant details (if any), and the deposit amount and tenure you want.

Step 3: Submit Your KYC Documents Along with the filled application, you need to submit a recent photograph, self-attested copies of your ID proof and address proof, and a copy of your self-attested PAN card.

Step 4: Make the Payment The deposit amount can be paid by cheque or NEFT in favour of “Sakthi Finance Ltd.” Cash is not accepted.

Step 5: Receive Your Deposit Certificate Once processed, you’ll receive a deposit certificate. Keep it safely — you’ll need it at maturity.

Step 6: At Maturity On maturity, the amount will be refunded by cheque or NEFT directly to your bank account, upon submission of the duly discharged deposit certificate.

Key Rules You Must Know Before Investing

A few important things to keep in mind before you commit:

Premature Withdrawal Rules: Deposits cannot be pre-closed before the expiry of 3 months. If you withdraw between 3 and 6 months, no interest is paid. If you withdraw after 6 months but before maturity, interest is payable but at a reduced rate as per RBI directives.

This is fairly standard across NBFC FDs, but it’s good to know going in. Don’t lock in money you might need urgently within 6 months.

Tax Deducted at Source (TDS): TDS applies as per Income Tax rules. If your interest income crosses ₹5,000 per year from an NBFC FD (threshold as per current IT rules), TDS will be deducted. You can submit Form 15G/15H to avoid TDS if your total income is below the taxable limit.

Interest Payout Frequency: Interest can be received monthly or quarterly for the fixed income scheme, with a minimum deposit of ₹25,000 for monthly payouts and ₹10,000 for quarterly or cumulative deposits.

Top Benefits of Investing in Sakthi Finance FD

Here’s a clean summary of why investors choose this option:

- Higher Returns: Rates up to 9.00% for regular investors and 9.25% for senior citizens — significantly above most bank FDs

- Flexible Tenures: Choose from 15 months to 60 months based on your financial goals

- Regular Income Option: Monthly or quarterly payouts make it ideal for retirees and people wanting passive income

- Compound Growth: The cumulative scheme offers solid compounding for long-term wealth building

- Established Track Record: Over 70 years in business with RBI-regulated NBFC status

- Joint Account Facility: Up to 3 joint applicants allowed

- Multiple Investor Categories: Open to individuals, firms, trusts, companies, and HUFs

- Senior Citizen Benefits: Extra 0.25% p.a. for senior citizens on all tenures

Who Should Invest — And Who Should Think Twice

Great fit if you are:

- A retiree wanting a reliable monthly income without market risk

- A salaried professional looking to park surplus funds for 3–5 years at better rates

- An HUF or small business wanting steady fixed-income returns

- A conservative investor who wants to beat inflation without equity risk

Think twice if you are:

- Someone who might need the money within 6 months (due to premature withdrawal restrictions)

- Someone whose entire savings would go into one NBFC FD (diversification is wise)

- Someone needing DICGC-insured deposits (bank FDs are safer from an insurance standpoint)

Practical Example: What Does Your Money Actually Earn?

Let’s run through a few quick examples so you can see the real numbers.

Example 1: Monthly Income Seeker (Retiree, ₹5 Lakhs, 60 Months)

- Investment: ₹5,00,000

- Rate: 9.00% p.a.

- Monthly Payout: ≈ ₹3,750/month

- Total Interest Earned over 5 years: ≈ ₹2,25,000

- Principal returned at maturity: ₹5,00,000

Example 2: Corpus Builder (Salaried Professional, ₹2 Lakhs, 36 Months)

- Investment: ₹2,00,000

- Rate: 8.75% p.a. (Cumulative)

- Amount at Maturity: ≈ ₹2,59,300

- Gain: ≈ ₹59,300

Example 3: Senior Citizen (60 Months, ₹3 Lakhs)

- Investment: ₹3,00,000

- Rate: 9.25% p.a. (Cumulative)

- Annual Yield: 11.59%

- Amount at Maturity: ≈ ₹4,73,910

- Gain: ≈ ₹1,73,910

The numbers speak for themselves — especially for longer tenure deposits where compounding has more time to work.

How to Contact Sakthi Finance

Want to get started or have questions? Here’s how to reach them:

- Toll-Free Number: 1800 1030 120

- Direct Number: 88709 33099

- Website: sakthifinance.com

- Investments Page: sakthifinance.com/investments

- Email: Available on the contact page of the official website (mail sakthifinance queries through their official contact form)

- Branch Network: 50+ branches across Tamil Nadu, Karnataka, Kerala, Andhra Pradesh, and Telangana

If you’re looking to invest, it’s always best to reach out to your nearest branch or authorised distributor — Sakthi Financial Services — for the most current forms and any updated rate information.

Tips to Maximise Your Returns with Sakthi Finance FD

Here are a few practical tips to make the most of your investment:

1. Go Longer for Better Rates The 48-month and 60-month options both offer 9.00% (9.25% for senior citizens) — locking in for longer pays off.

2. Choose Cumulative if You Don’t Need Monthly Income Compounding works best when you don’t disturb the principal or interest. Cumulative deposits deliver a significantly higher effective yield.

3. Ladder Your Deposits Instead of putting everything in one FD, spread across 15-month, 36-month, and 60-month deposits. This way, you have liquidity at regular intervals while still earning high rates.

4. Submit Form 15G/15H Proactively If your income is below the taxable threshold, submit the TDS exemption form at the start of every financial year to avoid unnecessary deductions and the hassle of filing for refunds.

5. Use Joint Accounts for Nomination Clarity Adding a joint applicant or clear nominee ensures smooth transfer in case of unforeseen circumstances — important for long-tenure deposits.

6. Don’t Invest Emergency Funds Here Given the premature withdrawal restrictions in the first 6 months, make sure you have a separate liquid fund or savings account for emergencies before investing in an NBFC FD.

A Word on Safety and Risk

Let’s address this honestly — because responsible investing means understanding both sides.

Sakthi Finance is a registered NBFC regulated by the Reserve Bank of India. They publish their investment details, comply with SEBI regulations for NCDs, and have a decades-long operating history.

However, unlike bank FDs, NBFC deposits do not carry DICGC deposit insurance. This means in the very unlikely event of default, there is no government-backed insurance to protect your deposit the way a bank FD would be protected up to ₹5 lakhs.

The way to manage this responsibly is to:

- Not concentrate 100% of your savings in a single NBFC FD

- Diversify across instruments — some in bank FDs, some in NBFC FDs, some in liquid funds

- Stick to NBFCs with long operating histories and transparent financials — Sakthi Finance checks both boxes

The higher rate is a reward for accepting slightly higher risk. The key is to invest wisely — not avoid the opportunity altogether.

Frequently Asked Questions (FAQs)

1. What are the current Sakthi Finance FD interest rates in 2026?

The Sakthi Finance FD interest rates currently stand at 8.25% p.a. for 15 months, 8.50% for 24 months, 8.75% for 36 months, and 9.00% for 48 and 60 months for regular investors. Senior citizens receive an additional 0.25% on all tenures. These rates have been in effect since August 2023 — always check the official website for the latest updates.

2. What is the minimum amount to invest in Sakthi Finance FD?

The minimum deposit amount is ₹10,000 for quarterly and cumulative deposit schemes. For the monthly interest payout option, the minimum deposit is ₹25,000. Amounts must be in multiples of ₹1,000 above the minimum.

3. Can I withdraw my Sakthi Finance FD before maturity?

Yes, premature withdrawal is allowed, but with conditions. No premature closure is permitted within the first 3 months. Between 3 and 6 months, the deposit can be closed but no interest is paid. After 6 months, interest is paid at a reduced rate as per RBI guidelines.

4. What is Sakthi Finance NCD and how is it different from an FD?

Sakthi Finance NCD (Non-Convertible Debenture) is a debt instrument that is listed on stock exchanges, making it tradeable. Unlike FDs which are held to maturity with the company, NCDs can be sold in the secondary market. NCDs typically offer fixed interest rates for a defined tenure and are a good option for investors comfortable with exchange-listed instruments.

5. How do I contact Sakthi Finance or reach them by mail?

You can reach Sakthi Finance through their toll-free number 1800 1030 120 or call 88709 33099. To mail Sakthi Finance, visit their official website at sakthifinance.com and use the contact form. You can also visit any of their 50+ branches across South India.

6. Is Sakthi Finance FD safe for senior citizens?

Sakthi Finance is an RBI-regulated NBFC with over 70 years of operational history, which makes it a relatively trustworthy option. Senior citizens also benefit from a higher rate of 0.25% extra on all tenures. However, as with all NBFC FDs, the deposits are not covered under DICGC insurance. Senior investors should ideally split their corpus between bank FDs (insured) and NBFC FDs (higher-yielding) for balanced risk management.

Conclusion: Is Sakthi Finance FD Worth It in 2026?

If you’re someone who wants more from your savings without venturing into market-linked investments, Sakthi Finance FD interest rates offer a compelling case.

At 8.25% to 9.00% for regular investors and 8.50% to 9.25% for senior citizens, the returns are well above what most bank FDs are offering. Add to that the flexibility of tenure, monthly/quarterly income options, and the credibility of a 70+ year old NBFC — and you have a solid fixed-income product worth considering.

Is it risk-free? No investment is. But for a calculated, smart allocation of your fixed-income portfolio, Sakthi Finance is a name that’s earned its place at the table.

Ready to take the next step?

Visit sakthifinance.com/investments to view the latest rates and download the application form. Or call their toll-free number 1800 1030 120 to connect with a representative who can walk you through the process.

Your money deserves better than a 6.5% bank FD. Give it a chance to grow.

Disclaimer: This article is for informational purposes only and should not be construed as financial advice. Interest rates are subject to change. Please verify current rates directly with Sakthi Finance Limited before investing. Consult a certified financial advisor to understand the suitability of this product for your personal financial situation.

Tags: Sakthi Finance FD interest rates, Sakthi Finance FD rates 2026, Sakthi Finance NCD, mail sakthifinance, NBFC fixed deposit India, best FD rates 2026 India, Sakthi Finance deposits, NBFC FD vs bank FD