Muthoot Finance FD Rates 2026: Earn interest rates upto 8.95%

Are you looking for a safe place to park your savings and earn guaranteed returns? If yes, you’ve probably already heard about fixed deposits (FDs). And if you’re exploring options beyond regular banks, Muthoot Finance FD rates 2026 might have caught your eye.

Muthoot Capital Services — part of the well-known Muthoot Group — offers some of the most competitive fixed deposit interest rates in the NBFC (Non-Banking Financial Company) space today. With rates going up to 9.35% per annum for senior citizens, this is hard to ignore.

In this guide, I’ll walk you through everything you need to know — from the current Muthoot Finance interest rate for fixed deposit, to who should invest, how the schemes work, what the risks are, and how to make the most of your hard-earned money.

Let’s get started.

What Is Muthoot Capital Fixed Deposit?

Before we get into numbers, let’s understand what we’re dealing with.

Muthoot Capital Services Limited is a registered NBFC regulated by the Reserve Bank of India (RBI). It is part of the Muthoot Group — one of India’s largest and most trusted financial conglomerates, primarily known for its gold loan business.

Like a bank FD, a Muthoot Capital FD allows you to deposit a lump sum amount for a fixed tenure. At the end of the tenure (or at regular intervals, depending on the scheme), you receive your principal back along with interest.

The key difference? NBFCs like Muthoot Capital often offer higher interest rates compared to many banks, making them attractive to investors chasing better returns.

CRISIL — one of India’s top credit rating agencies — has given Muthoot Capital an A+/Stable rating, which signals adequate safety in repaying depositors on time. This adds a layer of credibility to the investment.

Muthoot Finance FD Rates 2026 — Current Interest Rate Table

Now, let’s get to the part you’re really here for — the actual numbers.

The Muthoot Finance interest rate for fixed deposit 2026 varies based on the tenure, the type of scheme, and whether you’re a regular citizen or a senior citizen. Here’s a comprehensive breakdown:

1. Cumulative Deposits (Maturity Plan) — Annual Compounding

In this plan, the interest is compounded annually and paid along with the principal at maturity. This is ideal for people who don’t need regular income and want to grow their corpus over time.

| Tenure | Regular Citizens (% p.a.) | Senior Citizens (% p.a.) |

| 1 Year | 7.90% | 8.15% |

| 2 Years | 8.65% | 8.90% |

| 3 Years | 8.95% | 9.20% |

| 4 Years | 8.75% | 9.00% |

| 5 Years | 8.50% | 8.75% |

*(Rates updated as of February 2026)*

2. Non-Cumulative Deposits (Monthly Interest Plan)

This scheme is designed for people who want regular monthly income from their FD. The interest is paid every month directly to your bank account.

| Tenure | Regular Citizens (% p.a.) | Senior Citizens (% p.a.) |

| 1 Year | 7.65% | 7.90% |

| 2 Years | 8.00% | 8.25% |

| 3 Years | 8.50% | 8.75% |

| 4 Years | 8.60% | 8.55% |

| 5 Years | 8.50% | 8.75% |

*(Rates updated as of February 2026)*

3. Non-Cumulative Deposits (Annual Interest Plan)

Interest is paid once every year in this plan. It’s a middle ground — you don’t have to wait until maturity, but the payouts aren’t as frequent as the monthly plan.

| Tenure | Regular Citizens (% p.a.) | Senior Citizens (% p.a.) |

| 1 Year | 7.90% | 8.15% |

| 2 Years | 8.70% | 8.95% |

| 3 Years | 9.10% | 9.35% |

| 4 Years | 8.90% | 9.15% |

| 5 Years | 8.90% | 9.15% |

*(Rates updated as of February 2026)*

The highest Muthoot Finance interest rate for fixed deposit 2026 currently stands at 9.35% per annum — available to senior citizens under the Annual Interest Plan for a 3-year tenure.

3 Types of Muthoot Capital FD Schemes Explained

Muthoot Capital offers three distinct FD schemes. Let me break each one down in plain language:

Scheme A — Monthly Interest Plan

Under this scheme, you receive your interest income every month. If you’ve invested Rs. 5 lakh at 8.50% p.a. for 3 years, you’ll get approximately Rs. 3,542 deposited into your bank account every month. This is a great fit for retirees or anyone who wants their FD to act like a steady salary.

Scheme B — Annual Interest Plan

Here, the interest is credited once a year. You earn a lump sum interest amount at the end of each year. This works well for people who want periodic access to money without breaking the FD.

Scheme C — Cumulative Maturity Plan

This is the power of compounding at work. Your interest gets added back to the principal each year, and you earn interest on that growing balance. At the end of the tenure, you get the full maturity amount in one shot. If you don’t need the money in the short term, this is typically the best option to maximize your returns.

Key Features of Muthoot Finance FD

Here’s a quick summary of the important features you should know before investing:

- Minimum deposit amount: Rs. 1,000 only — extremely accessible for first-time investors

- Tenure: Ranges from 1 year to 5 years

- Renewal: Your FD can be renewed at maturity with fresh interest rates

- Loan against FD: You can borrow up to 75% of your deposit value (after the FD has been active for 3 months)

- Joint holding: Up to 3 people can hold a single FD jointly

- CRISIL Credit Rating: A+/Stable — indicating adequate financial safety

- Regulated by RBI as a registered NBFC

The low minimum deposit makes it particularly inclusive — even a first-time investor with limited savings can get started.

Practical Example: How Much Will You Earn?

Let’s put the Muthoot Finance FD rates to work with a real-life example.

Example 1 — Retiree Looking for Monthly Income

Mr. Sharma is a 62-year-old retiree from Delhi. He has Rs. 10 lakh to invest and wants a monthly income to supplement his pension.

He chooses the Monthly Interest Plan (Scheme A) for 3 years at the senior citizen rate of 8.75% p.a.

Monthly interest = (10,00,000 x 8.75%) / 12 = Rs. 7,292 per month

Over 3 years, he receives a total of approximately Rs. 2.63 lakh in interest income, while his principal of Rs. 10 lakh remains safe and is returned at maturity.

Example 2 — Salaried Professional Building a Corpus

Priya is a 35-year-old software engineer who wants to grow Rs. 3 lakh over 3 years without touching it.

She opts for the Cumulative Maturity Plan (Scheme C) at 8.95% p.a. for 3 years.

Maturity Amount = Rs. 3,00,000 x (1 + 0.0895)^3 ≈ Rs. 3,89,755

She earns approximately Rs. 89,755 in returns — all without any active management. Just deposit and forget.

Who Should Invest in Muthoot Finance FD?

Muthoot Capital FD is a great fit for:

- Retirees and senior citizens: Higher interest rates + monthly payout option = perfect for regular income needs

- Conservative investors: People who prioritise capital safety over high-risk, high-reward strategies

- Salaried professionals: Looking to park bonuses or savings for 1–5 years with guaranteed returns

- First-time investors: Low minimum investment of Rs. 1,000 makes it very beginner-friendly

- Parents saving for goals: School fees, college education, or a child’s future — predictable maturity amounts help you plan

If you’re the kind of person who says ‘I just want my money to be safe and grow steadily,’ this FD is made for you.

Muthoot Capital FD vs Other Popular Investment Options

Let’s put Muthoot Finance FD rates in context by comparing them with other common options:

| Investment Option | Approx. Returns | Risk Level | Liquidity | Tax Benefit |

| Muthoot Capital FD | 7.90% – 9.35% p.a. | Low | Low (lock-in) | No (80C not applicable) |

| SBI Bank FD | 6.50% – 7.10% p.a. | Very Low | Moderate | Yes (5-yr Tax Saver) |

| Post Office FD | 6.90% – 7.50% p.a. | Very Low | Low | Yes (5-yr) |

| Mutual Funds (Debt) | 6% – 8% p.a.* | Moderate | High | No |

| PPF | 7.10% p.a. | Very Low | Very Low (15 yr) | Yes (EEE) |

| Stock Market | Variable (10–15%*) | High | High | Partial |

*Past performance. Not guaranteed.

As you can see, Muthoot Capital FD offers noticeably higher returns than most bank FDs and government schemes, while maintaining a relatively low-risk profile. The trade-off is lower liquidity — so it’s best for money you won’t need urgently.

Loan Against Muthoot Finance FD — What You Need to Know

One of the lesser-known but very useful features of Muthoot Capital FD is the loan facility.

Here’s how it works:

- The FD must be at least 3 months old before you can apply for a loan

- You can borrow up to 75% of your deposit amount

- The loan interest rate is 2% higher than the FD interest rate you’re earning

- The final decision to grant a loan rests with Muthoot Capital

Let’s say you’ve invested Rs. 5 lakh in an FD at 8.95% for 3 years. After 3 months, you can apply for a loan of up to Rs. 3.75 lakh at an interest rate of 10.95%. This is still much cheaper than a personal loan from a bank (which typically starts at 12–15%).

This feature ensures your FD works doubly hard — it keeps earning interest while also acting as collateral for an emergency loan.

Premature Withdrawal Rules — Read Before You Invest

Life is unpredictable. What if you need your money before the FD matures?

Here’s what Muthoot Capital’s policy looks like for early withdrawals:

Withdrawal before 3 months:

Not allowed at all — except in the case of the depositor’s death.

Withdrawal between 3 and 6 months:

The principal is returned, but no interest is paid. In fact, if any interest was already paid out (in monthly or annual plans), it will be recovered from the principal.

Withdrawal after 6 months but before maturity:

Interest is paid, but at a rate 2% lower than the rate applicable for the period the FD actually ran. If no specific rate applies, the deduction is 3% from the minimum applicable rate.

The takeaway here is simple: Muthoot Capital FD works best when you commit to the full tenure. If there’s any chance you’ll need the money within 6 months, this might not be the right product for you. Always keep an emergency fund separately so your FD can run its full course.

How to Invest in Muthoot Capital FD — Step by Step

Getting started is simpler than you might think. Here’s a quick rundown:

Step 1 — Decide Your Investment Details

Choose the amount (minimum Rs. 1,000), tenure (1 to 5 years), and scheme type (Monthly/Annual/Cumulative) based on your financial goals.

Step 2 — Gather Your Documents

You’ll typically need: PAN card, Aadhaar card (for KYC), passport-size photographs, and a cancelled cheque for interest payouts.

Step 3 — Apply Online or at a Branch

You can visit the Muthoot Capital website or a nearby branch to apply. Many financial aggregator platforms also allow you to book Muthoot Capital FDs online.

Step 4 — Submit the Application and Funds

Complete the application form, submit documents, and transfer the investment amount. You’ll receive a Fixed Deposit Receipt (FDR) as proof of your investment.

Step 5 — Track and Renew

Keep track of the maturity date. You’ll have the option to renew at prevailing interest rates or redeem your investment.

Tax Implications on Muthoot Capital FD

Let’s address a question most investors have: How is FD interest taxed?

The interest you earn on Muthoot Capital FD is added to your total income and taxed according to your income tax slab. This is just like how bank FD interest is treated.

Additionally, TDS (Tax Deducted at Source) is applicable if your total interest income exceeds Rs. 5,000 in a financial year (for NBFCs). TDS is deducted at 10% if your PAN is registered, or at 20% if PAN is not provided.

You can submit Form 15G (for individuals below 60) or Form 15H (for senior citizens) if your total income is below the taxable limit, to avoid TDS deduction.

Note: Muthoot Capital FD does not offer the Section 80C tax deduction benefit unlike 5-year bank Tax Saver FDs. Keep this in mind while tax planning.

Key Tips Before Investing in Muthoot Finance FD

Here are a few practical pointers to help you invest smartly:

- Don’t put all your savings in one FD — stagger them across tenures (called FD laddering) to balance liquidity and returns

- Senior citizens should always check for the additional 0.25% benefit on rates — it adds up meaningfully over time

- Always compare rates across multiple NBFCs and banks before committing — rates change frequently

- Ensure you have a separate emergency fund (at least 3–6 months of expenses) so you never need to prematurely break your FD

- Submit Form 15G or 15H at the beginning of each financial year if applicable, to avoid unnecessary TDS

- Keep a digital copy of your FDR (Fixed Deposit Receipt) in a safe location

Muthoot Finance Interest Rate for Fixed Deposit 2026 — Quick Summary

Just in case you’re in a hurry, here’s the quick snapshot of the Muthoot Finance interest rate for fixed deposit 2026:

- Highest rate for general public: 9.10% p.a. (Annual plan, 3 years)

- Highest rate for senior citizens: 9.35% p.a. (Annual plan, 3 years)

- Minimum deposit: Rs. 1,000

- Tenure range: 1 year to 5 years

- Credit rating: A+/Stable by CRISIL

- Schemes: Monthly Interest, Annual Interest, Cumulative Maturity

- Loan against FD: Up to 75% of deposit amount

Frequently Asked Questions (FAQs)

Q1. What is the highest Muthoot Finance FD rate in 2026?

The highest Muthoot Finance FD rate in 2026 is 9.35% per annum, available to senior citizens on the Non-Cumulative Annual Interest Plan for a 3-year tenure. For regular citizens, the highest rate is 9.10% per annum on the same plan and tenure.

Q2. Is Muthoot Finance FD safe to invest in?

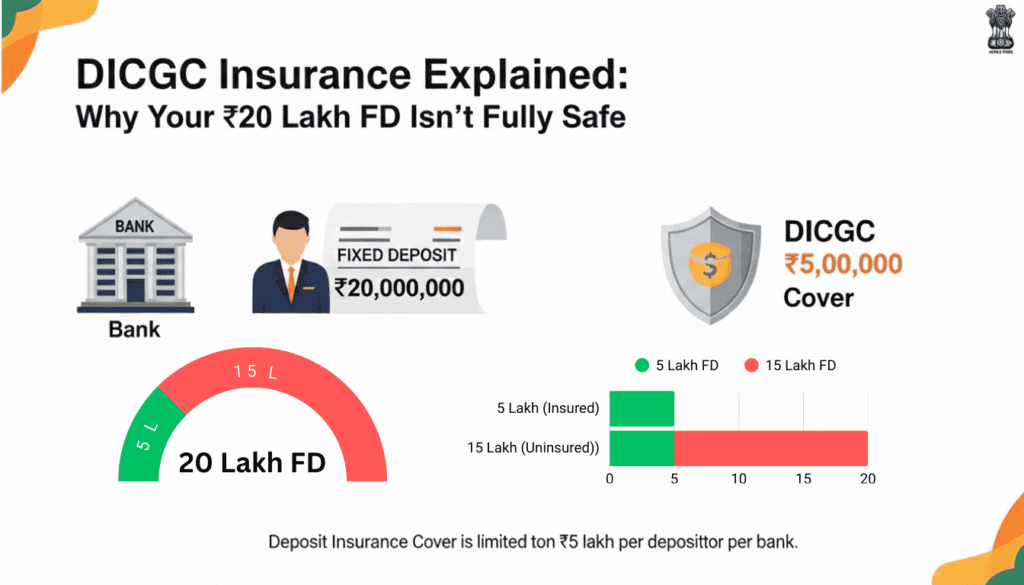

Muthoot Capital Services is a RBI-registered NBFC and holds an A+/Stable credit rating from CRISIL, which indicates adequate safety. That said, NBFC FDs are not covered under the DICGC insurance scheme (which protects bank deposits up to Rs. 5 lakh). Always assess your risk tolerance before investing.

Q3. What is the minimum amount to invest in Muthoot Capital FD?

The minimum investment amount is Rs. 1,000. This makes Muthoot Capital FD very accessible even for first-time investors or those with limited savings.

Q4. Can I get monthly income from Muthoot Finance FD?

Yes. Muthoot Capital offers a Monthly Interest Plan (Scheme A) under which interest is credited to your bank account every month. This is a popular option among retirees and senior citizens who rely on regular income.

Q5. What happens if I withdraw my Muthoot FD before maturity?

Premature withdrawal is not allowed in the first 3 months. Between 3–6 months, the principal is returned without any interest. After 6 months, interest is paid at a rate 2% lower than the applicable rate for the period the deposit ran.

Q6. Do senior citizens get extra interest on Muthoot Capital FD?

Yes, senior citizens (60 years and above) receive an additional 0.25% per annum over the regular citizen rates across all schemes and tenures. So a 3-year Cumulative FD that earns 8.95% for the general public earns 9.20% for senior citizens.

Conclusion — Is Muthoot Finance FD Right for You?

Let’s be honest — in today’s world, finding an investment that is safe, predictable, and delivers decent returns is not easy. That’s exactly where Muthoot Finance FD rates stand out.

With rates as high as 9.35% per annum for senior citizens and 9.10% for the general public, Muthoot Capital FD comfortably outperforms most bank FDs and even some government schemes. Add to that the flexibility of three different payout schemes, a low minimum deposit, and an A+ CRISIL rating — and you have a compelling product for conservative investors.

Whether you’re a retiree looking for monthly income, a salaried professional building a safety net, or a beginner just starting their investment journey — Muthoot Finance FD offers something for everyone.

Just remember the golden rules: don’t invest money you might need in the short term, always maintain a separate emergency fund, and consider spreading your deposits across tenures for better flexibility.

So, if you’re ready to put your money to work safely and smartly, Muthoot Capital FD is absolutely worth a serious look. Head to the Muthoot Capital website or a trusted financial platform to check the latest rates and start your application today.

Your money deserves to work as hard as you do.

Disclaimer: The interest rates mentioned in this article are based on data available as of February 2026 and are subject to change. Always verify current rates on the official Muthoot Capital website before investing. This article is for informational purposes only and does not constitute financial advice.